Economic curse words (nine letters, not four)

In the most recent Zillow Home Price Expectations Survey, we asked over 100 expert panelists to weigh-in re: their expectations for (CPI) inflation and economic recession in the U.S. The survey was conducted over a two-week period ended May 9th.

The I-word: Inflation

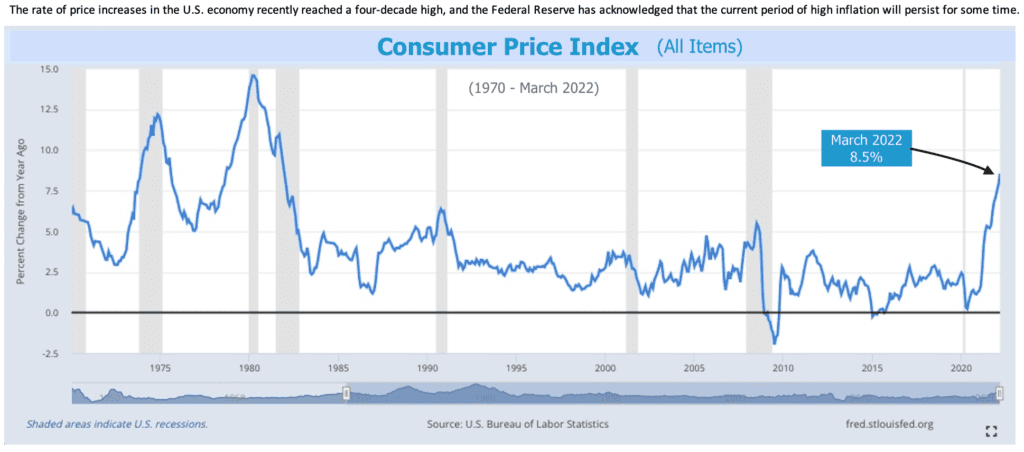

During the survey field period, the latest (March) CPI print was 8.5%–at the time, a four-decade high level. Here’s the question preamble presented to the panel:

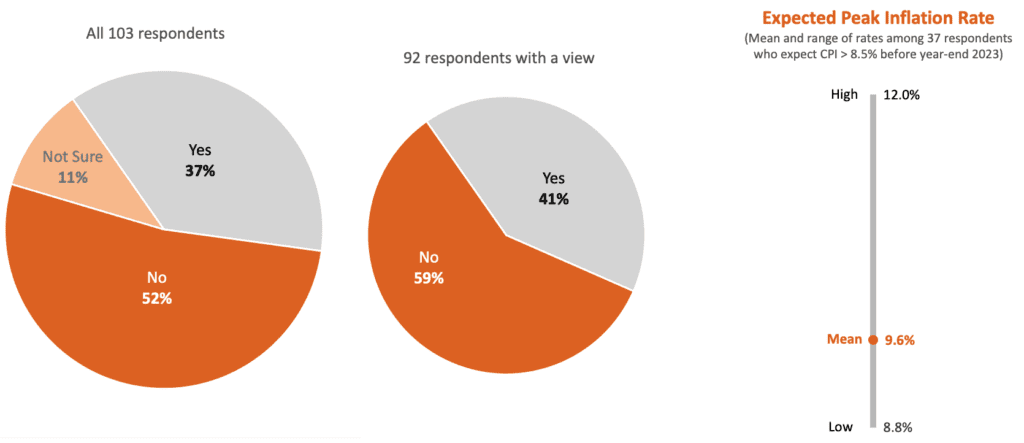

And here’s the question we asked: “The latest U.S. inflation reading (CPI annual rate, all items, as of March 2022) reached 8.5%. Do you expect this rate to rise above this level sometime before the end of 2023?” (Panelists who responded “Yes” were subsequently asked to indicate the peak inflation rate expected before year-end 2023).

More than 100 experts responded to this question. Here’s a summary:

On May 11th–two days after our survey closed–the Bureau of Labor Statistics announced that April CPI fell to 8.3%. Cue the “Still painfully high and persistent, but we’re beyond peak inflation” music (the Wall Street consensus estimate for May CPI was a flat 8.3% annual rate heading into this morning’s official release). Holy head-fake! Actual May CPI came in this morning at +1.0% MoM and +8.6% YoY, establishing a brand-new four decade high. Although it was a broad-based pop, the shelter, gasoline, and food index components contributed most to the increase.

Notably, optimistic narrators who’ve been highlighting the combination of very low unemployment, solid (but nominal!) wage growth, and strong consumer spending numbers paused this morning to digest the implications of this morning’s University of Michigan preliminary estimate of June consumer sentiment. The index fell to a record-low 50.2, down from the 58.4 level registered in May and the 58.1 consensus estimate. Although that survey is derived from a very small sample and is subject to revision later this month, there’s no doubt that consumers’ inflation expectations are ratcheting up, and likely becoming anchored at significantly higher levels.

The R-word: Recession

Here’s the question preamble presented to the panel:

In March, the Fed increased its benchmark interest rate from near zero by a quarter point–the first increase in more than three years. A week later, Chairman Jerome Powell summed up this way the desired outcome and goals of present Fed policy initiatives: “The economy achieves a soft landing, with inflation coming down and unemployment holding steady”. In early April, St. Louis Fed President James Bullard suggested that the Fed is “behind the curve”, and two weeks later, Chairman Powell said “50 basis points will be on the table for the May [FOMC] meeting”. Additional rate increases and incremental shrinkage of the Fed’s $9 trillion asset portfolio are the primary levers the central bank can pull to tame inflation–and to pull off, potentially, a soft landing for the U.S. economy.

The question:

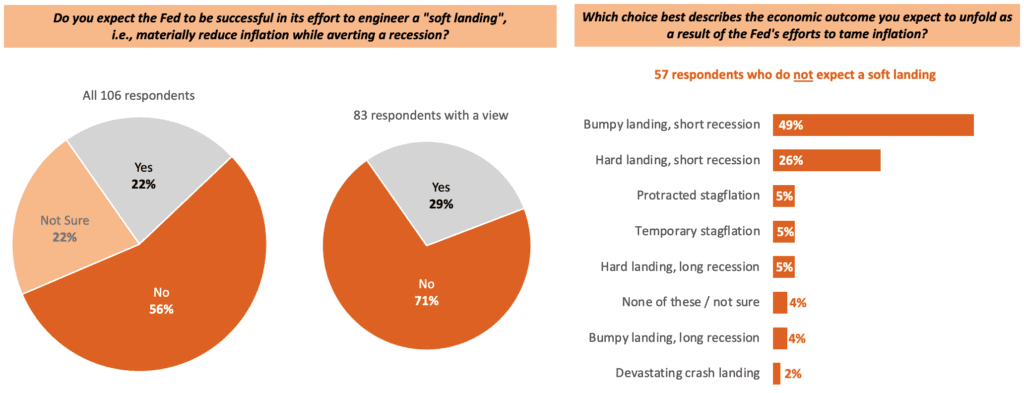

Do you expect the Fed to be successful in its effort to engineer a “soft landing”, i.e., materially reduce inflation while averting a recession? (Panelists who responded “No” were subsequently asked to select an answer choice that best describes the economic outcome expected to unfold as a result of the Fed’s efforts to tame inflation).

Once again, more than 100 experts responded to this question. Here’s a summary:

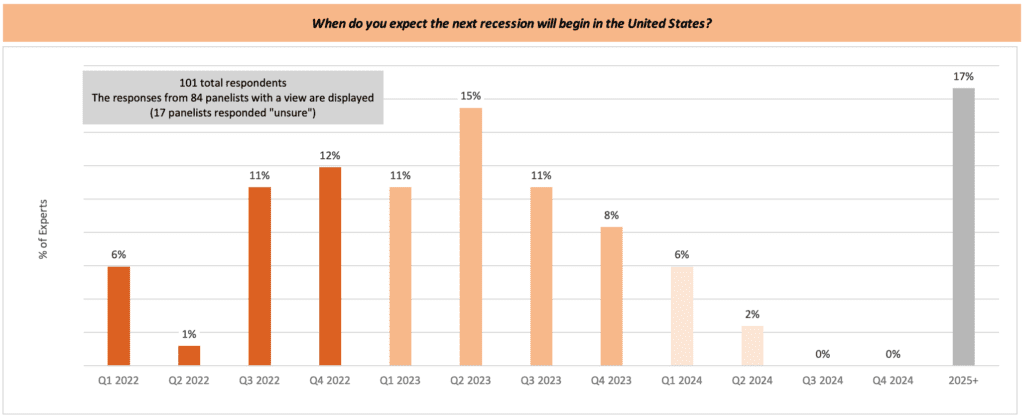

Finally, we asked the panel to predict when the next U.S. recession will begin:

A significant majority of experts expect a recession to begin sometime before the end of next year. Seatbelts buckled? Are you cursing yet?