The Quiet Erosion of Home Price Optimism

Home price expectations for this year remain nominally positive — but a softening consensus paired with the erosive effects of inflation tell a more sobering story. The latest (Q2 2026) edition of the Fannie Mae Home Price Expectations Survey, released today, revealed that half of respondents now expects real home prices to fall this year.

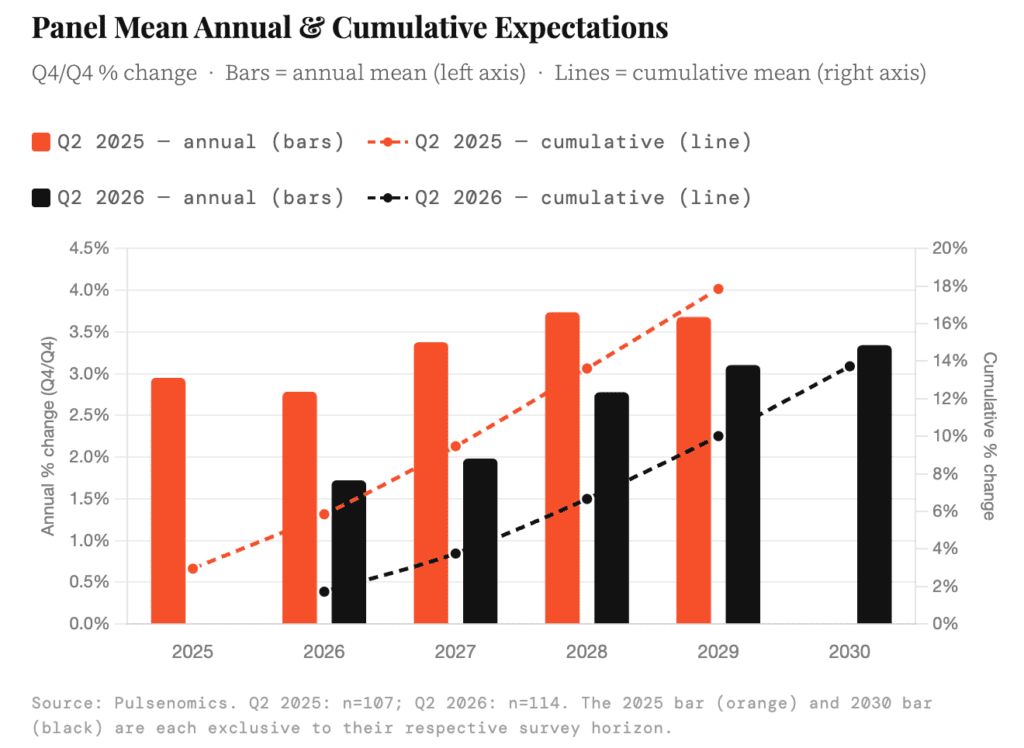

Ask most housing economists whether home prices will rise in 2026 and the answer is still yes — but likely with less conviction than a year ago. The Q2 2026 wave of Pulsenomics’ Home Price Expectations Survey, drawn from 114 economists and housing market experts, puts the panel’s mean forecast for annual home price appreciation at 1.7% — down from 2.8% twelve months earlier. That’s more than a full percentage point of optimism, quietly drained away.

The softening runs across every forecast year the survey covers, with 2027 registering the sharpest year-over-year decline in mean expectations — falling 1.4 percentage points below where it stood in the Q2 2025 survey. The cumulative five-year outlook has compressed in parallel: where last year’s panel projected a mean gain of 17.8% through 2029, this year’s panel sees just 13.7% through 2030 — a horizon that actually extends one year further.

The Direction of Travel is Clear

The chart above traces both the annual and cumulative trajectories from each survey wave. The pattern is unambiguous: in every overlapping forecast year from 2026 through 2029, the Q2 2026 mean sits below where Q2 2025 stood. The cumulative lines — which compound annual expectations into a running total — show the gap widening over time, as smaller annual estimates stack into materially lower multi-year projections.

At the individual level, the revision is nearly universal among panelists who participated in both waves. Of the 91 experts who participated in both (Q2 2025 and Q2 2026) survey waves, 67 (74%) lowered their 2026 outlook. Only 22 raised it. The average revision was −0.99 percentage points. The count of panelists projecting outright home price declines — a nominal forecast below zero — has grown from 8 to 12.

Nominal Gains, Real Losses

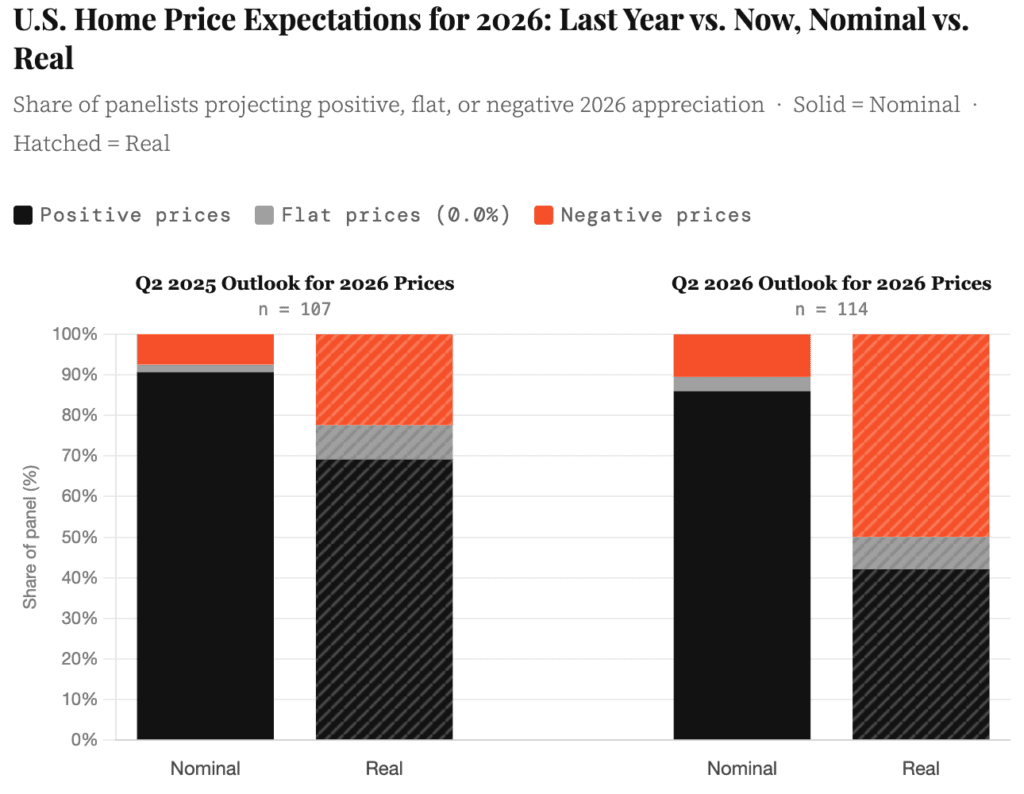

When these data are translated from nominal into real (inflation-adjusted) terms, the picture is more striking.

Using a 2% annual home price deflator (consistent with the Fed’s long-run inflation target and a bit lower than the December 2025 ex-shelter CPI reading of 2.4%), nominally positive forecasts can quickly become negative. A panelist projecting 1.5% nominal appreciation, for instance, is effectively forecasting that home prices will fall roughly half a percentage point in real terms.

On that inflation-adjusted basis, the YoY shift among experts is eye-opening. While 86% of Q2 2026 panelists project nominal gains, only 42% project real gains. The share expecting real home price declines is 50% — exactly half the panel — up from just over 22% on the same basis a year ago.

Wrap-Up

The consensus view heading into summer 2026 is not one of alarm — nationwide, nominal prices are still expected to rise, and the long-run cumulative projections remain positive. But the direction of revision, the breadth of downward movement among the experts, and the growing share of the panel in negative “real-terms” territory all point to cooling expectations and a thinning buffer between nominal gains and real losses.

Whether the softening trend in home price expectations continues — or whether fresh market developments through mid-year prompt a recalibration — will be worth watching in the coming months.